| Getting your Trinity Audio player ready... |

In the short term the whole sector is in a unique environment of extreme volatility with high initial margins, making physical trade very challenging exactly at the time when cocoa users need and want to contract physical volumes.

A series of indicators will be crucial to monitor for an indication of price direction. In our upcoming articles, we will explore these issues in greater detail. They include:

1. EUDR

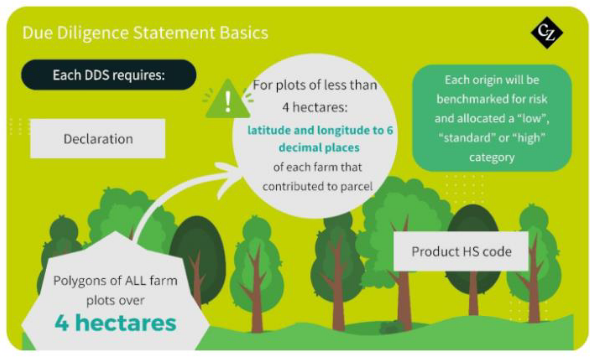

The exhausted cocoa industry is grappling with the European Union Deforestation Regulation (EUDR), which are set to enter into application on December 30, 2024 (barring any delays). This will require any cocoa crossing the EU customs border to be traceable to farm plot and compliant to the criteria of the regulation.

Read our article What EUDR Means for Cocoa to find out more.

2. Smuggling Activity

A clear understanding of the level of smuggling from Ivory Coast and Ghana during the 2023/24 crop is essential to understand the tree crop versus the arrivals at port/exports which might lead a correction in the assessed supply deficit. Next month, we’ll explore this issue in greater depth

3. Weather

The industry is watching the weather, particularly in West Africa, and its impact on the crop development for the 2024/25 crop. Another material deficit during the next crop would undoubtedly stimulate more buying.

4. Farm Gate Prices

The Ivory Coast and Ghana farm gate price announcement in early October will also influence participants’ thoughts on the direction of the market. Ivory Coast and Ghana have had to roll significant level of sales from the 2023/24 crop to the 2024/25 crop at low levels fixed before the price rally. Any 2024/25 sales were made a year forward — well before the highs on a backwardated market. This leads us to believe that a big farm gate price increase will be challenging.

The price was increased in both origins from around USD 1,550 for the main crop to USD 2,450 for the mid-crop. This level should at least be maintained for the 2024/25 main crop. This is less than half what the free-market origin farmers are receiving.

5. Grind Figures

The second quarter grind figures are also keenly awaited to see if demand is slowing. The complexity will be to assess whether the grind is affected by lower demand or lack of access to beans to grind.

These criteria include no risk of deforestation or illegal growing according to the land of production. This can encompass a range of issues, from land rights to labour rights, human rights, indigenous people, tax and corruption.

There are question marks over whether the supply chain will be able to prove compliance to EUDR for the entire volume required for Europe in time bearing in mind the due diligence needs to have been completed by the 2024/25 main crop in October.

It would be very risky to assume that there will be a delay in the regulation start date. Even if the regulation is pushed back, this won’t be announced until September/October, at which point it would be too late to start due diligence activities if it is not delayed.

So, the final big question to confront the industry is, what influence will EUDR have on price over and above the existing sensational market?